What are the fees involved in buying a second-hand property in Singapore?

When buying a second-hand property in Singapore, in addition to the purchase price itself, there are also some other fees to be paid. This article provides a quick overview of the relevant details.

Sale and Purchase Price

The purchase price includes the down payment (including the deposit) and the loan. The minimum down payment is 25% of the total purchase price.

Stamp Duty

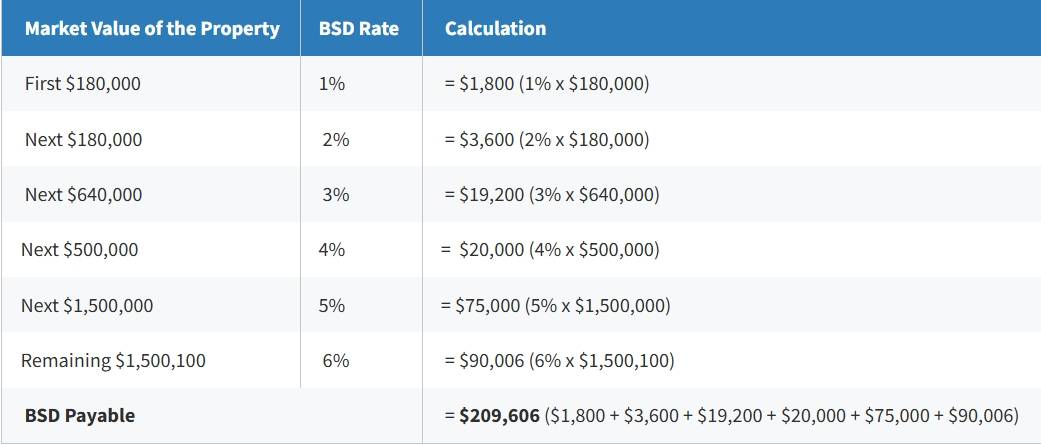

BSD - Buyer's Stamp Duty

BSD is a tax paid on documents signed when you buy or acquire property located in Singapore. Regardless of the buyer’s profile or number of residential properties owned by the buyer, it needs to be paid, and the amount is only affected by the value of the property itself.

Calculation Method:

BSD is computed based on the higher of the property price (as stated in the signed sales and purchase agreement) and the market value (as stated in the property's valuation report), with a progressive tax rate applied, and the total tax payable is the sum of the taxes in each bracket.

Example: A terrace house was purchased on 17 Feb 2023 at $4,500,100 which reflects the market value.

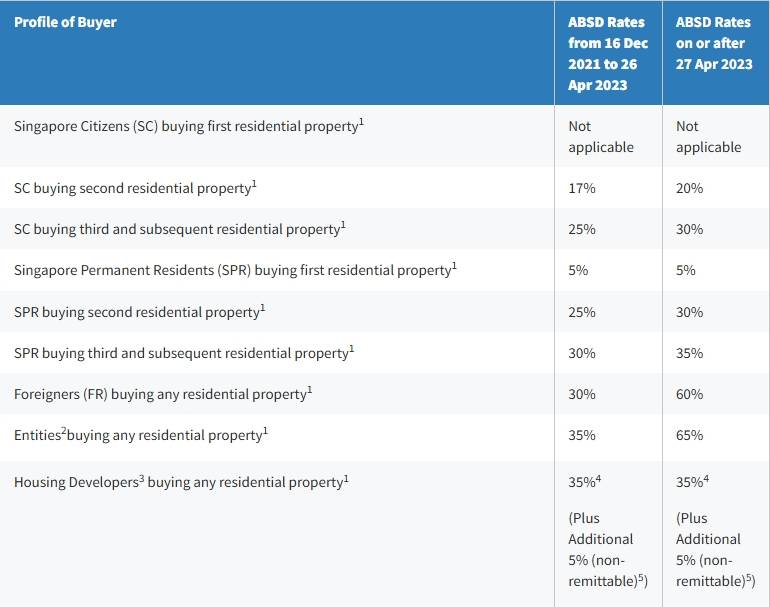

ABSD - Additional Buyer's Stamp Duty

Whether ABSD needs to be paid and the amount of payment are affected by factors such as the buyer’s profile and the number of residential properties owned by the Buyer. The details are as follows in the table.

Legal Fee

Lawyers will be responsible for reviewing the property's title status to ensure that there are no property rights disputes, mortgages, or other issues. At the same time, lawyers will also assist homebuyers in reviewing and signing the sales and purchase contract, explain terms in the contract to safeguard the legitimate rights and interests of homebuyers. For example, lawyers will carefully examine documents such as the property's title certificate and land deed, and check key terms such as the payment method, the delivery date of the property, and the delivery conditions of the property.

The legal fee will vary depending on the complexity of the transaction, such as the type of property, the type of transaction, the value of the property, whether a loan is needed, whether a trust needs to be established, etc. The fee is generally around S$2,000 - S$5,000.

Valuation fee

For the purchase of second-hand private properties where the bank requires an evaluation of the property's value, the bank will appoint its own appraiser to value the property, but the bank usually subsidizes this part of the fee, and the buyer does not need to pay it. If the buyer is purchasing the property in full, then the valuation fee needs to be paid by the buyer, which is approximately around S$300 - S$400.

In the case of purchasing an HDB flat while requiring an HDB loan, the buyer usually needs to pay a handling fee of S$120 to the relevant authority, which will appoint an appraiser to value the property.

Property appraisers will consider many factors such as the property's location, age, renovation condition, and market conditions to determine the property's value, providing homebuyers with a reasonable price reference to ensure that homebuyers do not buy the property at an overly high price.

Agent Fee

The agency fee for second-hand property transactions is usually paid by the seller. The seller pays the agreed agency fee to the seller's agent (except for HDB flats, where both the buyer and the seller usually pay their own fees in HDB transactions). If the buyer has their own buyer's agent to assist with the property purchase, then the buyer's agent and the seller's agent will negotiate the commission sharing ratio. For example, the market standard commission for second-hand property transactions is usually 2% + GST. If the buyer's agent and the seller's agent negotiate and agree to share the commission at the common ratio of 50%:50%, then after the transaction is successful, each of the buyer's and seller's agents will receive 1% + GST as the agency fee (paid by the seller). If the buyer does not have an agent, then the seller's agent will collect the full 2% + GST.

Some buyers who are not familiar with the market, if they DIY the entire property purchase process, may actually end up harming their own interests. Therefore, it is recommended that buyers, when they do not need to pay the agent fee themselves, find an agent to represent their interests, who will negotiate prices from the buyer's perspective, and help them control all aspects of the transaction throughout the process. Especially for buyers with tight cash flow, they should pay special attention to the requirements regarding payment methods and timelines.

The buyer's agent will help homebuyers find suitable properties, arrange property viewings, provide property ma rket information and property analysis, assist homebuyers in negotiating with sellers, dutifully liaise with banks and lawyers, and assist with the handling of relevant procedures. With their professional knowledge and rich experience, they can provide homebuyers with many valuable professional services, saving buyers money, time, effort, and worry. So, why not do it?

Read More

《Tenants must see:Singapore Tenancy Agreement and Key Terms》

《First-Time Purchase Guide: Eligibility requirements to buy a house and Property Types in Singapore》

《Singapore Rental Guide: Easily Find Your Ideal Home》

1

1 0

0 1

1

发表评论